June 2026 Florida Reinsurance Renewals

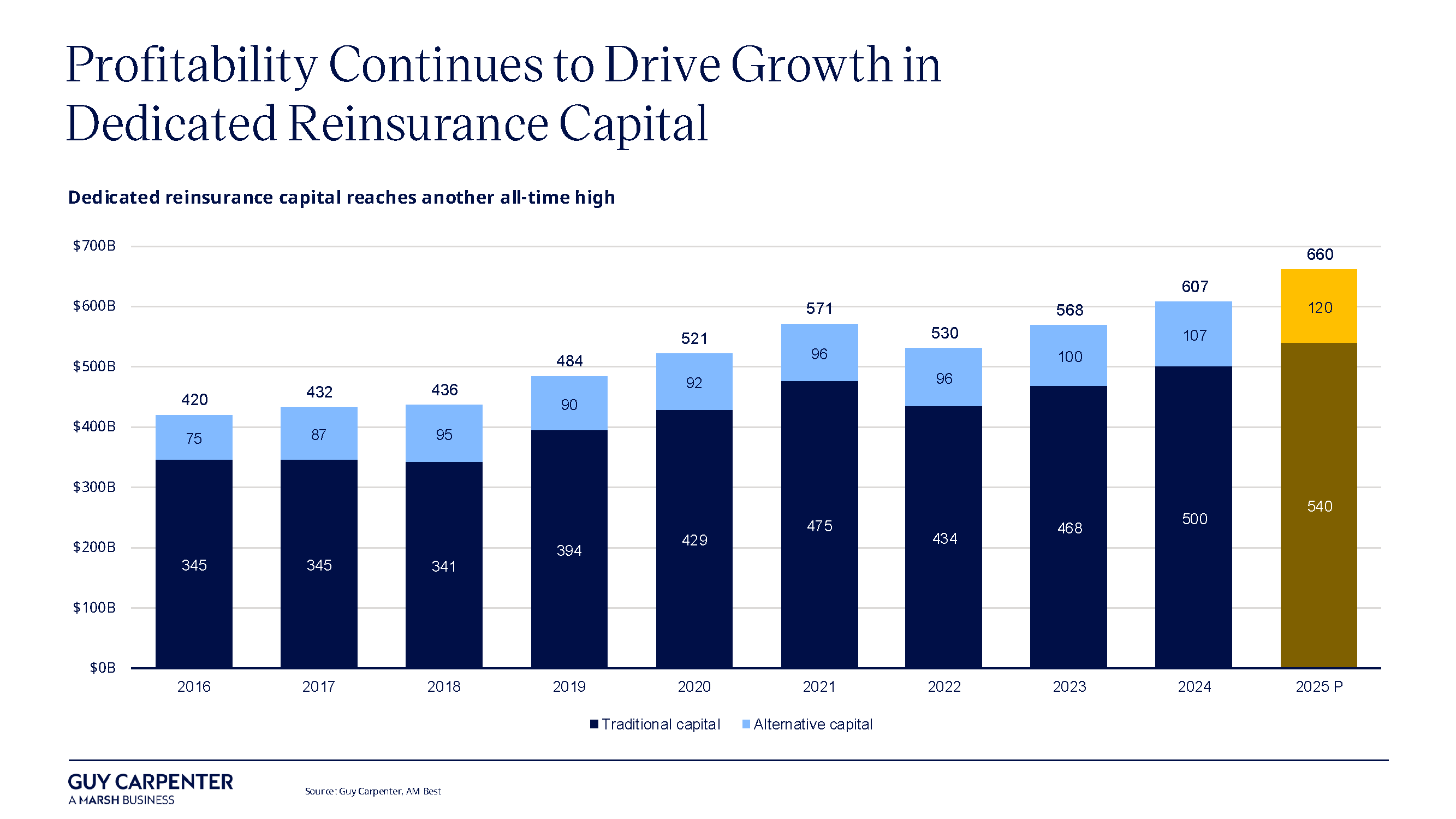

A Thriving Market Restoring Capital to Healthy Levels

We found that legal reforms, improved building resilience, and disciplined underwriting have combined to restore capital and confidence in the Florida market. That restoration is visible in the way insurers and reinsurers approached the June renewals — more capacity was available, terms improved, and pricing moved in line with the better loss outlook, which ultimately supports sustainable rate relief for policyholders.

Key themes from the report are:

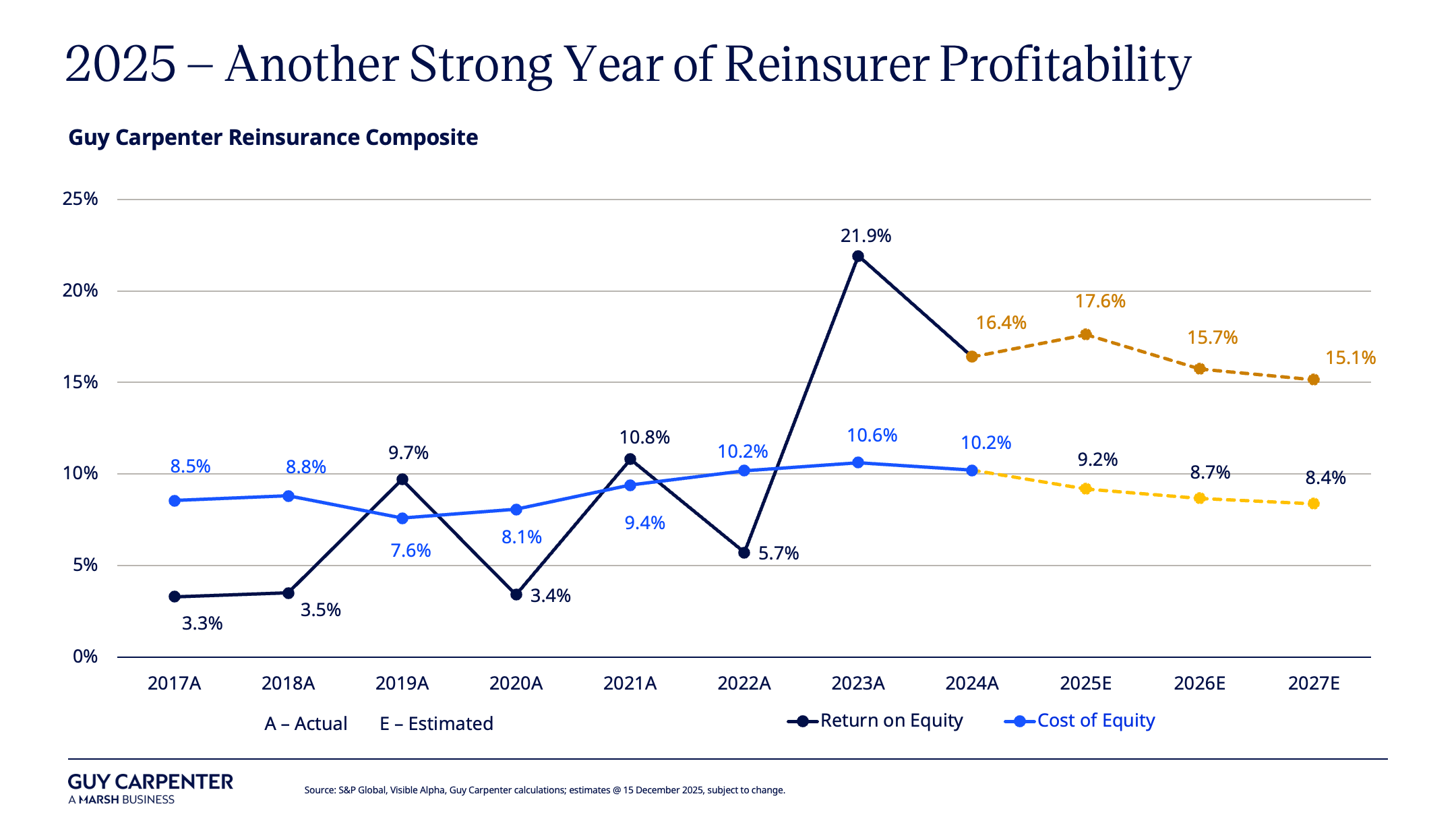

- Strong results by Florida carriers in 2025 set the stage for the June 2026 renewal season.

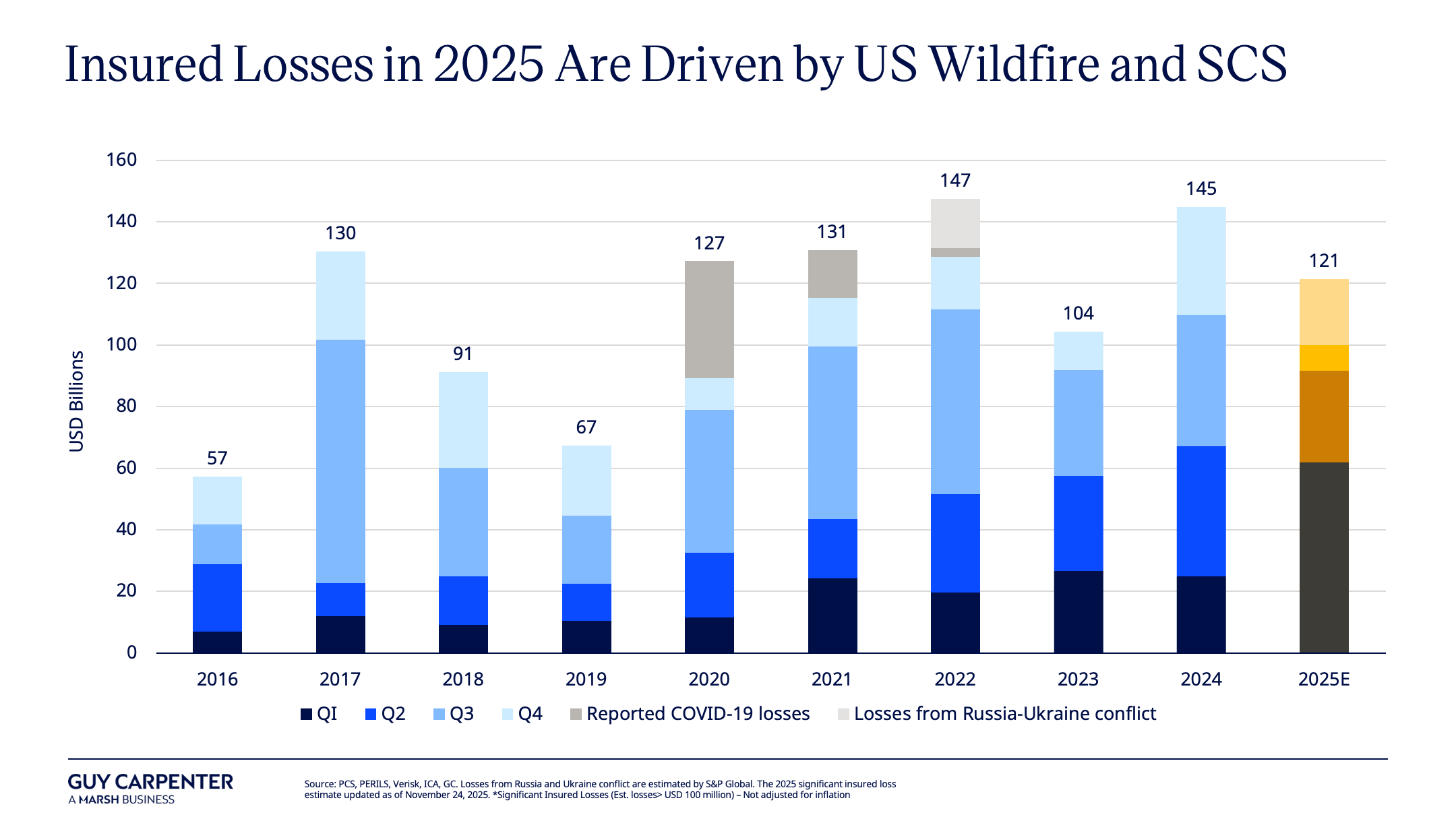

- Reduced hurricane losses and legal reforms have improved the view of risk for the state.

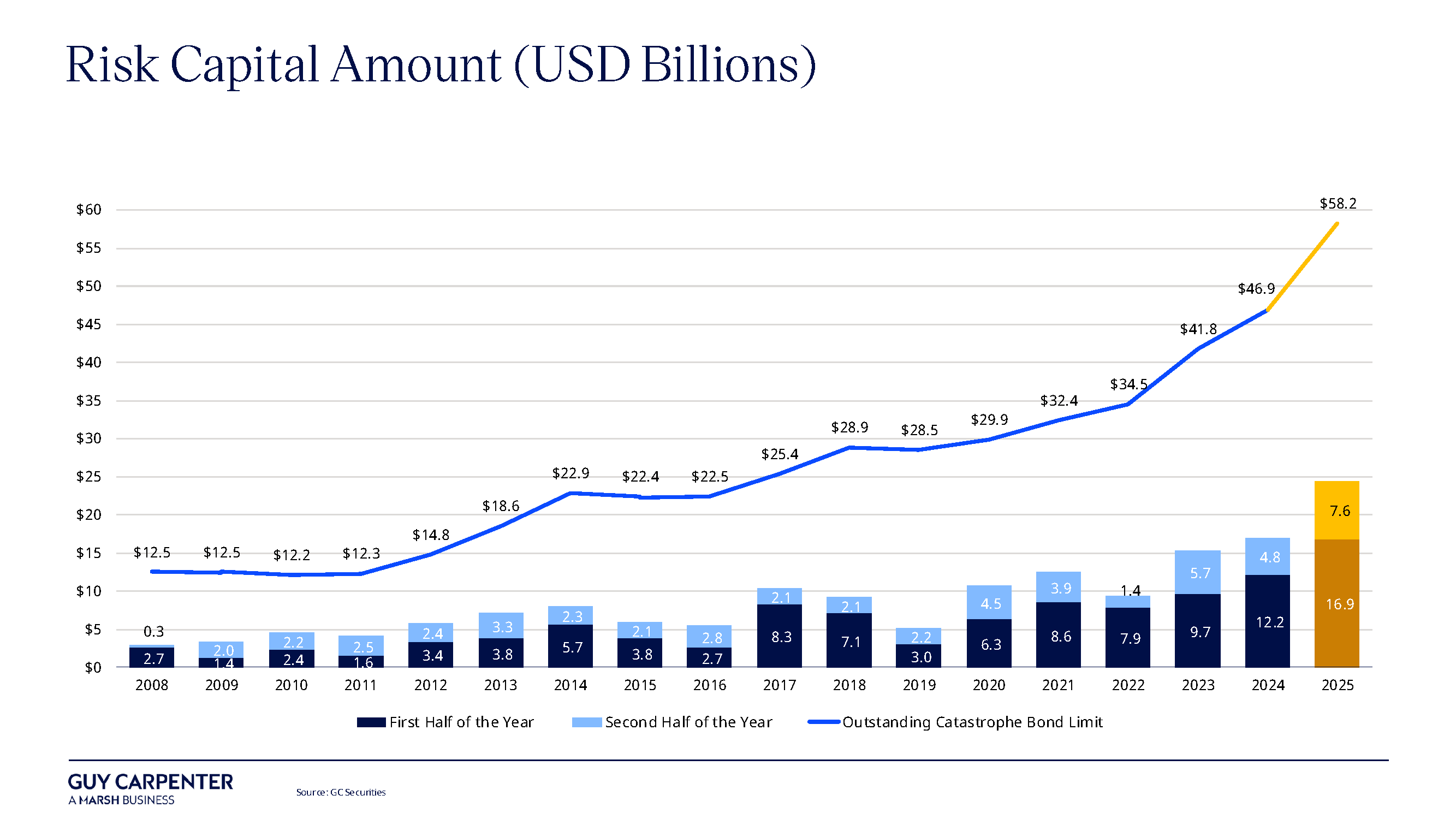

- There is increased demand for reinsurance and ILS capacity.

- Forecasted El Niño conditions are leaning toward a below-average to near-normal 2026 Atlantic hurricane season.